When money is tight before payday, the choice often comes down to cash advance apps vs payday loans. Both can cover a short gap, yet they work very differently and cost very different amounts. So in this guide, we’ll compare the two, look at popular apps like Bree, Nyble, and KOHO, and help you pick the cheaper, safer option. Quick note: CashPicks is an independent comparison platform, not a lender, and we don’t earn anything from the apps mentioned here.

Cash advance apps vs payday loans: the quick answer

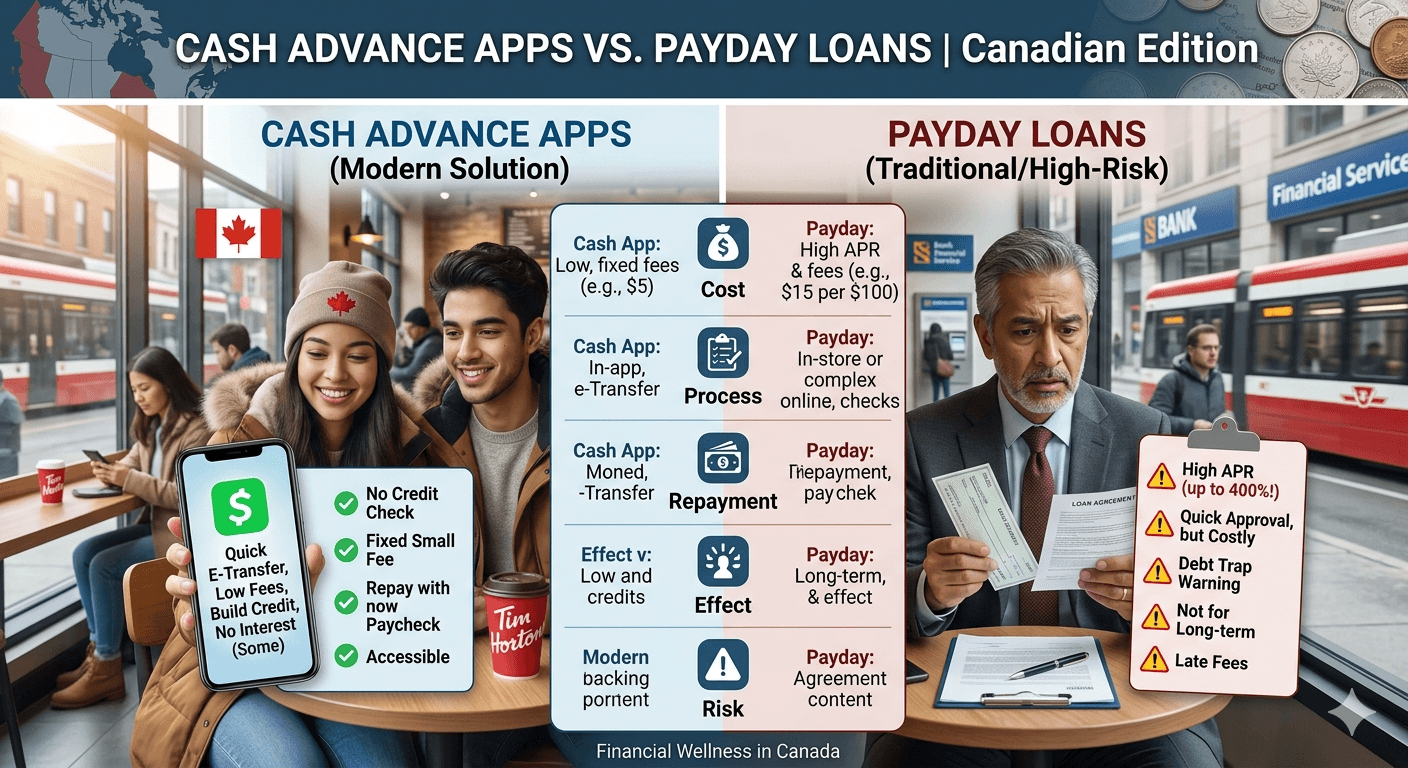

Here’s the short version. A cash advance app lets you draw a bit of pay you’ve already earned, usually with no interest and only a small or optional fee. A payday loan, on the other hand, is a regulated short-term loan that costs $14 for every $100 borrowed. As a result, for small amounts, an app is often the cheaper choice.

Still, the right pick depends on how much you need and how fast. So let’s break down each one.

How cash advance apps work

Cash advance apps give you early access to wages you’ve already earned, then collect the money on your next payday. Because they charge 0% interest, the cost is usually just a small flat fee, a monthly membership, or an optional tip. In addition, most don’t run a credit check, and many don’t charge NSF fees if a payment fails. That makes them a gentler option for a minor shortfall.

How payday loans work

A payday loan is a licensed, regulated loan of up to $1,500, repaid within 62 days. The cost is capped at $14 per $100, and that cap covers all fees. So a $300 loan costs $42, and a $500 loan costs $70. You can confirm the rules on the Financial Consumer Agency of Canada site, or check any amount with our payday loan calculator.

Cash advance apps vs payday loans, side by side

This comparison sums up the main differences at a glance. Cash advance apps vs payday loans: the key differences in Canada.

| Feature | Cash advance apps | Payday loans |

|---|---|---|

| Typical cost | 0% interest; small or optional fee | $14 per $100 (all fees) |

| Amount | About $20 to $750 | Up to $1,500 |

| Repayment | Next payday; often flexible | Full amount by next payday |

| Credit check | Usually none | Usually none |

| Speed | Minutes to hours | Often same day |

| Regulation | Lightly regulated (0% interest) | Licensed and capped by province |

Fees and limits change — check each provider. CashPicks is not a lender.

Bree, Nyble, and KOHO: a quick look

These three names come up the most, so here’s how they differ. Fees and limits change, though, so always check the app before you rely on it.

- Bree: Offers an interest-free advance of up to about $750, with no mandatory fee on standard delivery. You only pay extra if you want an instant transfer, and it accepts many income types.

- Nyble: Provides a smaller advance of around $250 and focuses on credit building, since it reports your payments to Equifax. A monthly plan unlocks instant transfers.

- KOHO: Its “Cover” feature offers a small interest-free advance of up to about $250, but you need a KOHO account and a low monthly subscription to use it.

Which should you choose?

Start with the amount. If you only need a small top-up, a cash advance app is usually cheaper and more flexible. However, if you need closer to $1,000 or more in one go, a payday loan may be the only option that covers it. Meanwhile, if you have a little time, the payday loan alternatives in Canada guide covers even cheaper routes, such as a credit union loan.

Whatever you pick, the same rule applies: borrow only what you can repay on time, and free help is available from Credit Counselling Canada if money feels tight. So it helps to read our responsible borrowing guide first, and if you’re worried about approval, our bad-credit payday loans guide explains what lenders actually check.

Staying safe either way

A few habits protect you with both options. First, never pay an upfront fee to “release” a loan, because that’s illegal in Canada and a classic scam. Next, skip any service promising “guaranteed approval,” which we cover in our no refusal payday loans guide. Finally, share details only through the official app or the lender’s secure site, and never your passwords.

Bottom line

In short, when it comes to cash advance apps vs payday loans, apps usually win on cost for small amounts, while payday loans cover larger, one-off needs. So match the choice to what you need, check the fees, and borrow only what you can repay. When you’re ready, compare licensed lenders on CashPicks and weigh every option.