Wondering about the real payday loan cost Canada charges these days? You’re in the right place. Since 1 January 2025, the rules are clear and the maths is simple. So in this guide, we’ll show exactly what a $300 and a $500 payday loan cost, how the fee works, and what your equivalent APR looks like. We’ll keep the numbers plain and honest. Quick note: CashPicks is an independent comparison platform, not a lender.

How the payday loan cost in Canada is set

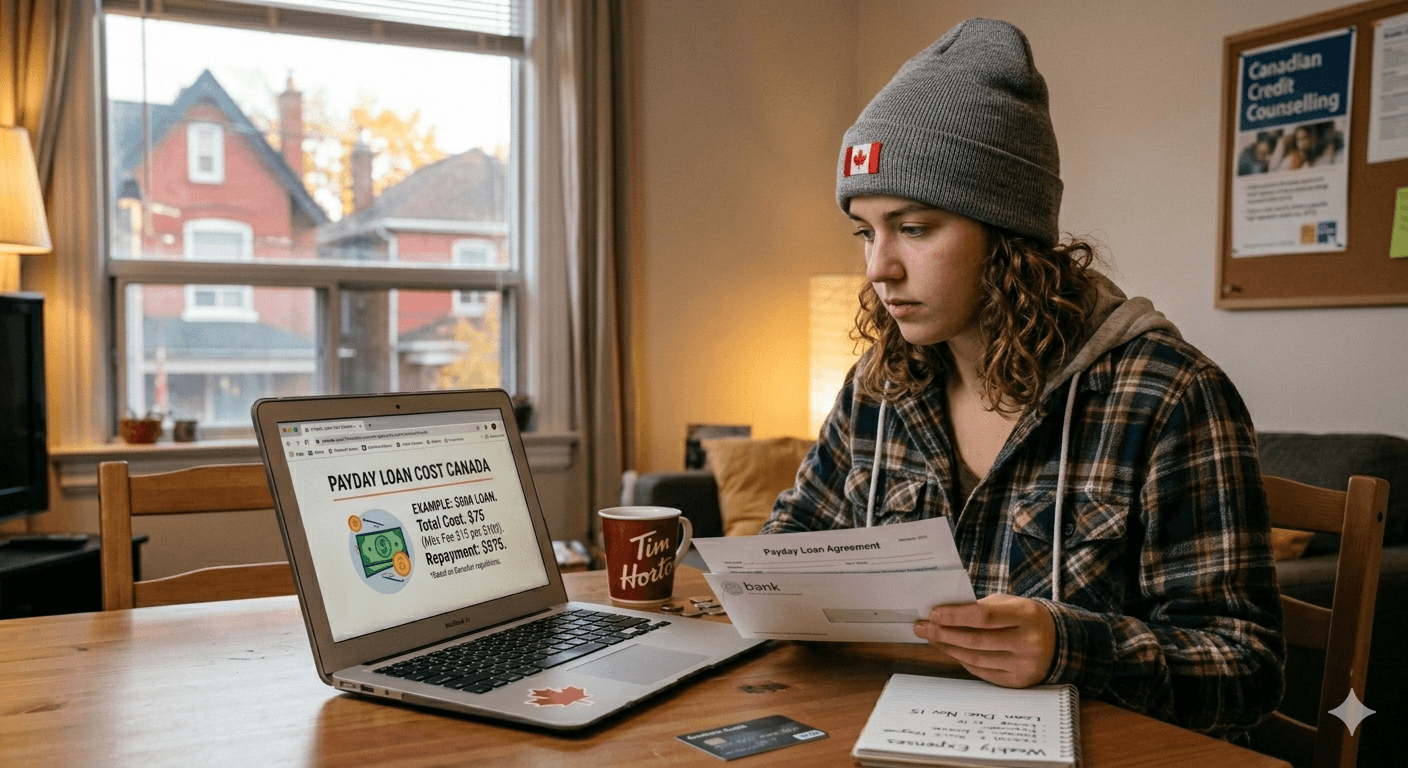

First, the rule that drives everything. Federal law caps the cost of a payday loan at $14 for every $100 borrowed, and that cap covers every fee combined. In other words, there are no hidden add-ons on top. So if you borrow $100, the most it can cost you is $14, which means you repay $114 in total.

Because the fee is a flat amount, the cost scales neatly with the size of the loan. For example, $200 costs $28, and $400 costs $56. You can read the basics on the Financial Consumer Agency of Canada website, which explains the cap in plain terms.

How much does a $300 payday loan cost?

Let’s start with a common amount. At $14 per $100, a $300 payday loan costs $42 in fees. As a result, you repay $342 in total on your due date. That’s the most a licensed lender can charge, so a quote higher than $42 on a $300 loan is a warning sign. The Ontario government shows similar cost examples.

How much does a $500 payday loan cost?

Now the other popular amount. A $500 payday loan costs $70 in fees, which means you repay $570 in total. Again, that figure includes everything, so there should be no surprise charges layered on afterward. If a lender adds “processing” or “insurance” fees on top, walk away.

Payday loan cost in Canada at a glance

Here’s the full picture so you can see the payday loan cost Canada borrowers face for any amount up to the $1,500 limit.

Payday loan cost in Canada at $14 per $100 (reviewed 2026). Try the numbers yourself with our calculator.

| You borrow | Fee ($14/$100) | Total to repay |

|---|---|---|

| $100 | $14 | $114 |

| $200 | $28 | $228 |

| $300popular | $42 | $342 |

| $500popular | $70 | $570 |

| $1,000 | $140 | $1,140 |

| $1,500 | $210 | $1,710 |

Costs reflect the federal $14 per $100 cap (all fees included) and can change. CashPicks is not a lender — confirm the exact cost before you borrow.

Want to test your own amount? Our payday loan calculator shows the fee, the total, and the due date instantly.

Why the APR looks so high

You may have seen payday loans quoted with an eye-watering APR, sometimes around 365%. So why is that, when the fee is “only” $14 per $100? The answer is the short term. APR is an annual figure, yet a payday loan usually lasts about two weeks. Therefore, stretching a two-week cost across a full year makes the percentage look huge.

Here’s the key takeaway. The dollar cost of a single, short payday loan is small and fixed. However, the cost adds up fast if you keep rolling loans over, because you pay the fee again each time. That’s exactly why payday loans suit a one-off gap, not a long-term shortfall.

Watch out for extra charges

One more thing to budget for. If your repayment bounces, the lender can charge a one-time fee of up to $20, and your bank may add its own NSF charge on top. So before you borrow, make sure the money will be in your account on the due date. For a fuller picture of the rules where you live, see our guide to the payday loan rules by province.

Is it worth it? Compare first

A payday loan can help in a genuine pinch, and now you know the exact cost. Even so, it’s an expensive way to borrow compared with a line of credit or a credit union loan. So before you commit, it’s smart to weigh your choices. You can compare licensed lenders on CashPicks, and our responsible borrowing guide covers cheaper alternatives worth a look.

Bottom line

In short, the payday loan cost Canada sets is simple to work out: $14 per $100, all in. A $300 loan costs $42, and a $500 loan costs $70. So check the exact figure with our calculator, confirm the lender is licensed, and compare your options on CashPicks before you borrow.